Your Next Customer May Never Visit Your Website

A customer opens their banking app and tells its assistant: "Find travel insurance for a two-week trip, and put it on whichever card earns the best rewards." The assistant reads dozens of policies, weighs cover against price, checks which card maximises points, and comes back with three ranked options. The customer compared nothing themselves.

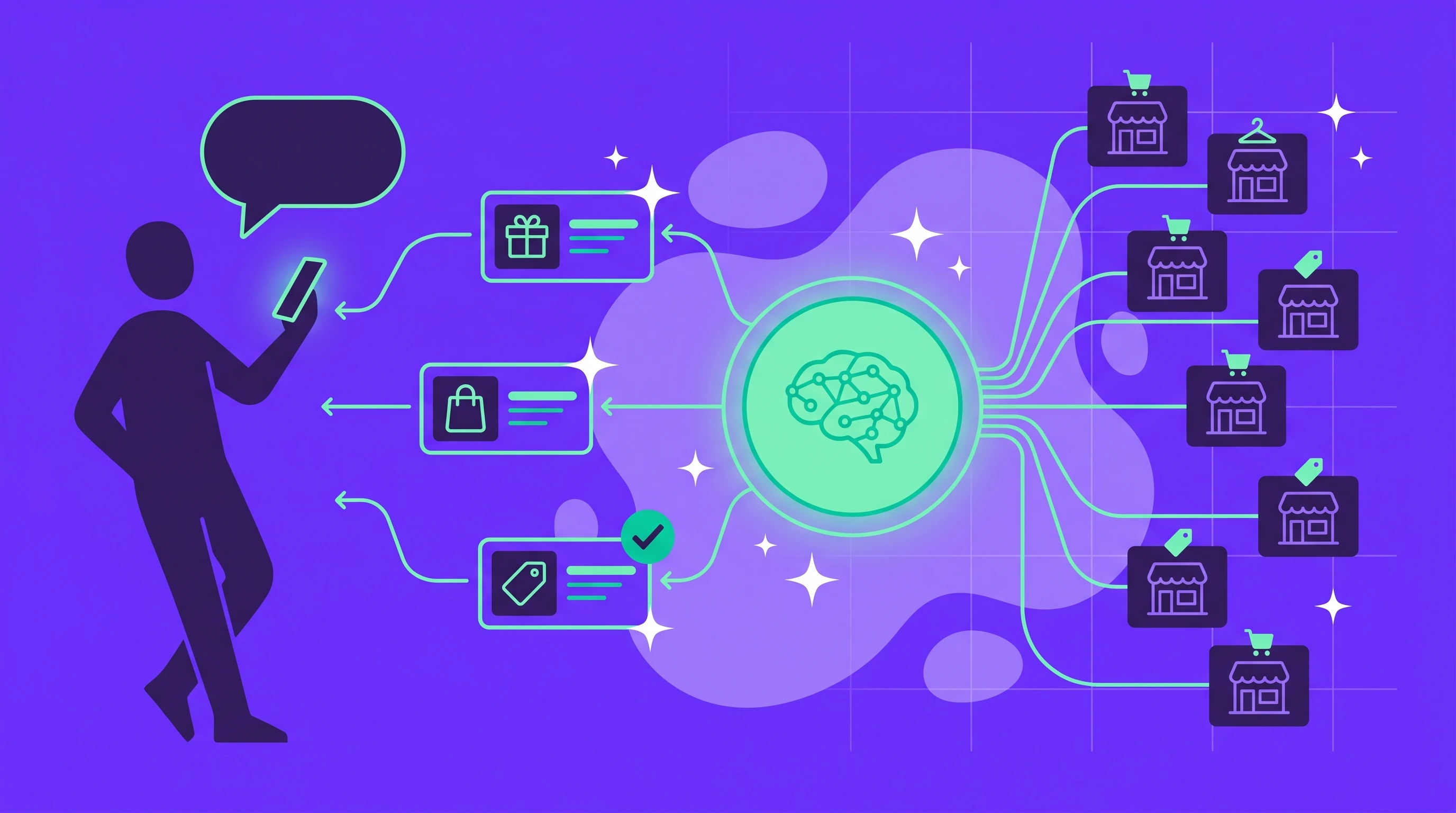

The same pattern is showing up in everyday retail, too. "I need an outfit for a summer garden wedding," answered minutes later with "Out of 27 offers reviewed, these are the three I recommend." This is agentic commerce: software that handles discovery, comparison, and parts of the transaction on a customer's behalf. Watch how the flow plays out:

This is not a far-future thesis. In late 2025 OpenAI and Stripe shipped Instant Checkout inside ChatGPT on an open Agentic Commerce Protocol, with Etsy, Walmart, and Shopify. Visa introduced its Trusted Agent Protocol and tokenised agent payments, Mastercard launched Agent Pay with live authenticated transactions, and Google published an Agent Payments Protocol backed by Mastercard, PayPal, and American Express. "Agent-authorised payments" here means tokenised credentials that let an agent pay within limits the customer sets, without ever handling raw card details. The infrastructure is arriving ahead of demand: by one industry estimate, only around 4% of consumers currently let AI complete a purchase autonomously. That gap is precisely the window to prepare in.

The first thing to evaluate your offer may not be a buyer or a search engine. It may be software acting for the buyer, and it only forwards what it can read, trust, and transact against.

AI assistants are becoming a new distribution layer

For two decades, digital strategy assumed a human would eventually land on a page, read it, and decide. Ranking, ads, UX, and brand all optimised for that moment of human attention.

When an agent does the discovery and comparison, that assumption weakens. Visibility stops being about ranking on a page a person reads and starts being about whether your offer is legible to the software doing the shortlisting. The journey shifts from customer → store toward customer → agent → merchant, and increasingly the customer may not see the storefront at all. The commercial consequences are concrete: exclusion from the consideration set, margin pressure from machine-led comparison, and a contest over who controls checkout, financing, and loyalty at the moment of purchase.

Two questions every business now has to answer

- Can an external agent discover, evaluate, and transact with your offer? If your catalog, pricing, and terms are only legible to a human reading a rendered page, an agent comparing dozens of options will quietly skip you. Inclusion in the shortlist now depends on being machine-readable and transactable.

- Do you want to own the interface, or supply the rails? When an agent sits between the customer and every merchant, there are three positions to take: own the customer-facing assistant, provide the infrastructure other agents depend on, or compete as a commodity selected largely on price. The first two are strategies. The third happens by default.

Where banks actually have an edge

Banks do not automatically win this shift, and trust alone is not enough. The general, day-to-day assistant is more likely to belong to the platforms and device makers already in front of the customer. But banks control assets that matter precisely when an agent moves from discovery to transaction: verified identity, recorded consent, payment authorisation, real-time account and budget context, fraud and risk controls, and dispute resolution.

That gives them a credible role in two forms. In specific, financially anchored journeys, where credit, rewards, or risk decide the outcome, a bank's own assistant can be the customer-facing agent. More broadly, the surer play is to provide the rails, identity, consent, and payment authorisation, that every other agent depends on. The institutions that choose which role they want, deliberately, will shape where they sit in the new flow rather than discover it after the fact.

The part most agentic-commerce talk skips: consent, audit, and liability

In regulated environments, this is not just an interface change. Before an agent can recommend, authorise, or execute a purchase, an institution has to answer the questions its risk and compliance teams raise first: Who authorised the agent, and for what? What can it do without explicit confirmation? How is consent recorded and revoked? Who is liable when an agent gets it wrong? How is the decision logged and audited, and what customer data may it use under privacy rules? Agentic commerce that ignores permissioning, auditability, fraud control, and clear liability will not pass a bank's second meeting.

What "agent-ready" means in practice

Preparing is concrete engineering, not a slogan. We frame it as four properties your offer needs, in order:

- Discoverable. Structured product, price, and eligibility data an agent can retrieve directly, not scrape from a rendered page.

- Understandable. Clear, machine-parsable attributes, terms, fees, availability, and disclosures, so an agent can reason about your offer instead of guessing.

- Permissioned. Identity, consent scopes, authentication, and transaction controls, so an agent acts only within what the customer and the regulator allow.

- Transactable. Agent-facing endpoints for the full path, search, quote, reserve, pay, confirm, cancel, with auth and rate limits built in. (Agent-to-agent, or A2A, simply means these calls happen between two pieces of software rather than through a human-facing screen.)

The strategic choice ahead

The question is not whether agents will replace every customer journey. It is whether your products can be discovered, evaluated, and transacted safely when software becomes the first evaluator, and whether you intend to own that interface or power it.

At 10Clouds Financial Institutions we help businesses make their offers discoverable, understandable, permissioned, and transactable for agents, and we help banks decide where to own the interface and where to supply the rails.