5 FinTech development trends for 2021

Over the past decade, FinTech has been steadily growing in popularity, and it's fair to say that it’s probably about to enter its golden age. 2020 was a year of such fast-paced evolution that it’s difficult to condense the changes down into one paragraph. Buy now pay later (BNPL) grew exponentially over the past twelve months, consolidation swept the industry with big dollar transactions, (with Visa purchasing Plaid and Mastercard buying Finicity among others) and there was a peaking institutional interest in crypto. China pressed ahead with its plans to issue a digital currency, and

Several American tech giants, including Google, Amazon and Uber are all embarking on financial projects. Fintechs such as Zelf and PayKey are turning messaging apps and phone keyboards into banking apps. At the same time, startups including Klarna, Checkout.com and Fast are capitalising off the new FinTech reign with valuations and initial public offerings (IPOs).

So what will the future hold for 2021? In 10Clouds’ traditional style, I have ranked my predictions in order from the most to the least likely of being adopted. Let's check in at the end of the year and see how many of these came true!

1. The emergence of FinTech as a service platforms

Forbes talks about their being an imbalance in the market at present with many FinTechs “wanting to partner with banks—but few banks are equipped to partner with the fintechs.” Enter fintech-as-a-service platforms.

What is FinTech as a service (Faas)? Many Fintechs are offering their APIs to businesses in the sector as software to be integrated into their systems. This model is relatively new but it is already evident that it will be rapidly growing in popularity.

Using a Fintech-as-a-service platform means that finance companies can optimise their end-to-end process, ensuring effective and fast-paced service provision online and on demand.

FaaS platforms ensure full management and deployment of delivery environments. Importantly, they also provide legal compliance with banking regulations and with proper security mechanisms such as strong authentication.

The path to integration is fraught with challenges for mid-sized banks which want to partner with FinTechs—resources to develop partnerships are limited, integrating into the core is a massive job, and developing other approaches from the very beginning is very time-consuming. But positive change in this area is already happening.

Karol Stępień, Head of Banking & FinTech at 10Clouds says: Another scenario here includes providers concentrated solely on delivering the fintech-like infrastructure as a service for separate banking ventures. This kind of services help banks simply to create their own fintechs way more effective then building them in-house from scratch. This approach limits also the ideation, research, delivery and deployment risks, shortening the go-to-market time at the same time.

2. More digital-only banks

The start of the pandemic meant a total eradication of the physical processes involved in banking. Accessing and managing personal funds became something that could only be done remotely and many conventional banks are still partly unprepared.

A McKinsey study revealed that digital payment is up there with the biggest fintech products. New generation financial institutions solved the emerging challenge by leveraging fintech solutions. They were able to offer convenient digital-only banking services removing the need for physical interaction.

There will be increasingly more digital institutions which will provide fully remote services, which is great news of course for consumers.

Alex Valdes, CTO and EVP of Trust Stamp says: “Customer experience demands are evolving, especially with newer generations. These customers want convenience and speed. They have less interest in building personal relationships with staff at a bank, and less time in their schedule to handle these tasks in person.”

This is a really interesting moment for banking representatives who contact clients on a daily basis. These positions may now evolve more towards the professional advisory sales model supported with the most innovative technology” says Karol Stępień.

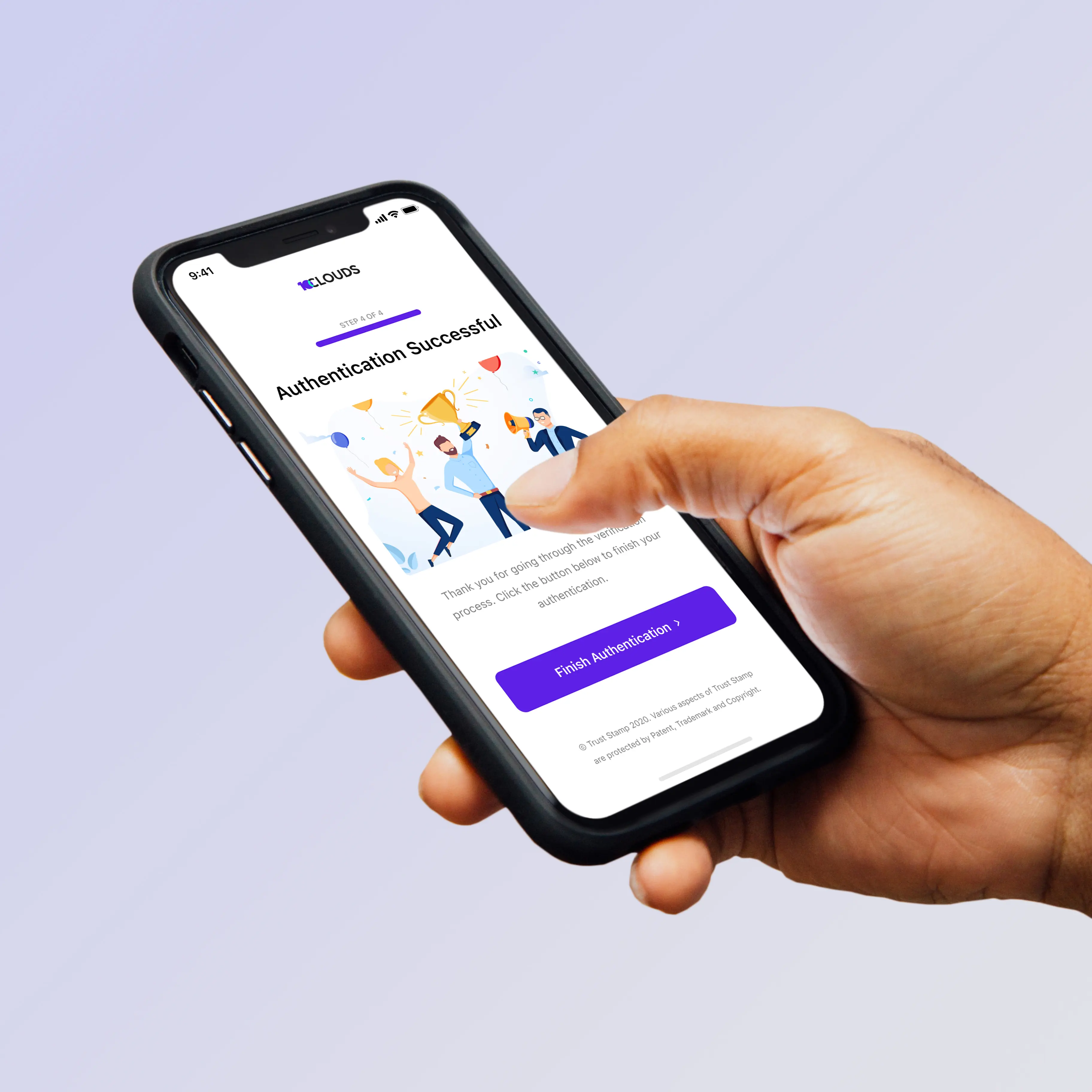

3. Wider use of biometric security systems

With the rise of digital-only banks, we will see an even greater increase in the need for biometric security systems. Cybercrime continues to be a real issue, and well implemented biometric solutions can provide the answer to this threat.

Alex Valdes, CTO and EVP of Trust Stamp says: “Biometric authentication has made it possible to do what humans have been doing for thousands of years with our eyes, which is recognizing the characteristics of one’s face to identify who they are.”

Due to the ongoing pandemic, biometric sensors that involve physical contact are forecast to drop in popularity, giving way to contactless solutions. We’ve entered an era in which all you’ll need to access your bank account, or even to open a new one, will be a phone, tablet or PC equipped with a camera, and some form of officially recognized ID. This is why we are so pleased to be working with Trust Stamp on the future of biometric authentication.

Apart from security, another major challenge that biometric authentication solves is user friction. As security measures become more advanced, there is more scrutiny which causes more friction for the customer, ultimately producing a negative impact on the overall customer experience.

But, as Alex Valdes points out, “with new technology, this belief has been challenged and even flipped on its head. For example, by coupling biometrics with automated ID validation, not only is security-enhanced through the use of sophisticated machine learning techniques to identify fraud but now the customer can save a trip to the bank, does not have to stand in a long line, and can do all of these steps from the comfort of their own home.”

Through automation, small things like extracting the personal details from the customer’s ID to prefill the rest of their application will save them additional time and headache, resulting in greater satisfaction.

4. The rise of autonomous finance

Autonomous finance is predicted to be increasingly popular this year. Why? Because it saves people time and allows them to focus on what’s important. Many banking clients find it difficult to stay on top of their financial admin, including utility bill payments, insurance, TV subscription, and more.

Autonomous finance takes the burden off consumers’ shoulders and automates the financial decision-making process with the use of Artificial Intelligence (AI) and Machine Learning.

But, autonomous finance requires a shift in how organizations approach operations as it means that they will have to fully digitize their processes. The pandemic has accelerated the pace of change in this area and has led to the rise of digital-only banks, which takes us onto the next point.

5. More effective big data management

Banks and fintechs of all sizes continue to hold considerable amounts of private data on clients. At present, much of this data is in an unstructured form and needs to be processed using powerful business analytics tools. These tools can be used to create valuable trend reports which show the potential identified risks.

At the same time, there is the structured data found on forms, including mortgage and loan applications, and even basic bank statements. Banks need to find more efficient ways of managing this big data.

At the moment, the financial service industry is at the forefront of investment in Big Data technologies. Several major banks are already using Big Data techniques to uncover new opportunities, but others are still lagging behind. Here’s where FinTechs will help.

“There are already existing solutions which could leverage business banking, but many financial institutions are shy in using them on a larger scale. A good example is data enrichment based on PSD2 AIS services for credit process improvement. These solutions may help in assessing the credit risk from the bank's perspective much more efficiently than in the traditional credit process - thanks to fresh information about client’s transactions. At the same time, it is potentially streamlining the process from the client perspective.” - says Karol Stępień.

FinTech developers are able to improve the processing of data through building apps which automate data extraction. Specially designed data algorithms can be used to quickly identify different data types and sort through them for analytical purposes, but note that there are some challenges to this process. Some documents will be in a file format that’s difficult to read or might be damaged. There are existing solutions to these issues in the form of software integrations which enable documents to be streamlined and cleaned up. These are likely to evolve further and be more commonly used in 2021.

So there you have it - our FinTech trend predictions for 2021. Now all we need to do is check in at the end of the year to see how many of these came true.

Looking for an experienced team to bring your digital product to life?

Get in touch for a free consultation on hello@10Clouds.com. Our friendly team will get back to you within one working day!